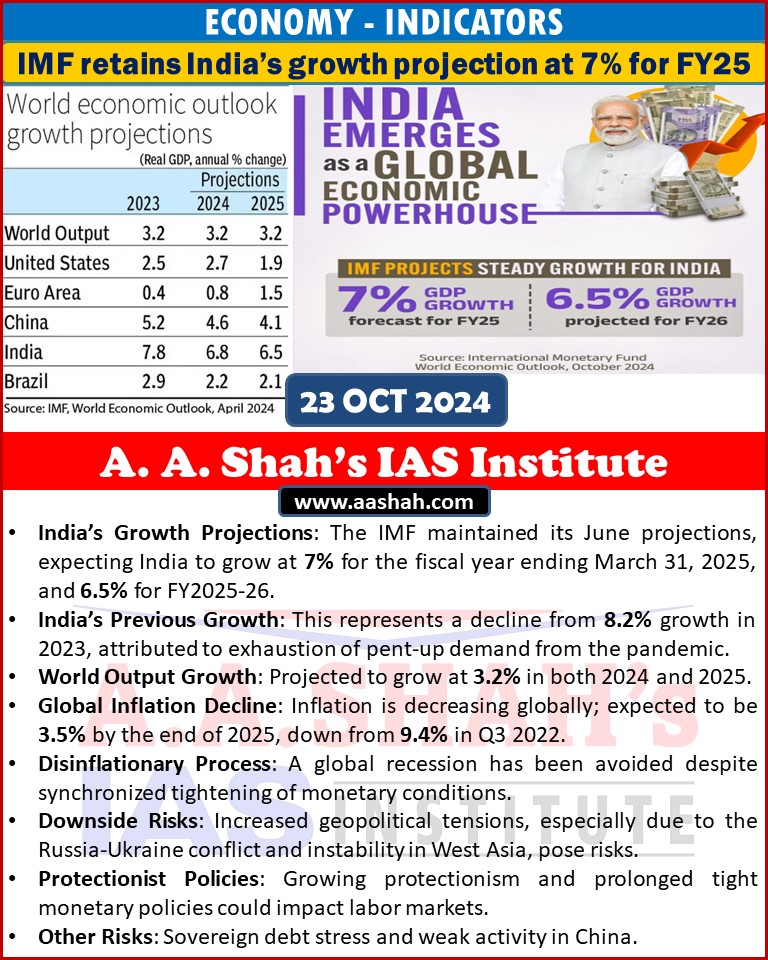

•India’s Growth Projections: The IMF maintained its June projections, expecting India to grow at 7% for the fiscal year ending March 31, 2025, and 6.5% for FY2025-26.

•India’s Previous Growth: This represents a decline from 8.2% growth in 2023, attributed to exhaustion of pent-up demand from the pandemic.

•World Output Growth: Projected to grow at 3.2% in both 2024 and 2025.

•Global Inflation Decline: Inflation is decreasing globally; expected to be 3.5% by the end of 2025, down from 9.4% in Q3 2022.

•Disinflationary Process: A global recession has been avoided despite synchronized tightening of monetary conditions.

•Downside Risks: Increased geopolitical tensions, especially due to the Russia-Ukraine conflict and instability in West Asia, pose risks.

•Protectionist Policies: Growing protectionism and prolonged tight monetary policies could impact labor markets.

•Other Risks: Sovereign debt stress and weak activity in China.

•Triple Policy Pivot: The IMF recommends:

1.Neutral Monetary Policy: Transitioning to a neutral stance, already underway in many nations.

2.Fiscal Buffers: Building fiscal buffers after years of loose fiscal policies.

3.Structural Reforms: Implementing reforms to enhance growth and productivity, address demographic changes, tackle climate transition, and increase resilience.

•The neutral stance is generally adopted when both inflation control and economic growth are given equal priority, allowing for adjustments in either direction as new information arises.

•It maintains a balanced focus, placing equal weightage on managing inflation while also supporting economic growth